Payday lending: significant financial harms

Payday loans in Louisiana carry annual percentage rates (APR) of interest averaging 400%. These high-cost loans are marketed as quick solutions to a financial emergency. Research shows, however, that payday loans typically lead to a cycle of debt that is nearly impossible to escape. The average payday customer in Louisiana ends up in 9 loans per year, which belies the industry’s claim that their loans are useful as short-term emergency boosts. Eighty-seven percent of payday loans made in Louisiana are made within two weeks of a previous loan being repaid. Payday lenders collect 75% of their revenue from borrowers caught in more than 10 loans per year, showing that the business model of payday lenders is based on repeat borrowing, not the one-time assistance they advertise.

Payday loans create a dangerous trap that keeps struggling folks in cycles of debt. They routinely drain hundreds of dollars from a person’s bank account in amounts well above the original loan amount. They are linked to a cascade of financial consequences, such as increased overdraft fees, delinquency on other bills, involuntary loss of bank accounts, and even bankruptcy.

In Louisiana, payday lenders drain more than $145 million in fees annually, and the vast majority of payday lenders operating in Louisiana are headquartered out of state. This fee drain hampers asset-building and economic opportunity in the Louisiana communities most impacted by these predatory lending practices.

The Solution: HB 675

Louisiana can cap payday loans at a 36% annual percentage rate (APR) to stop the debt trap. HB 675 will replace Louisiana’s Deferred Presentment and Small Loan Act to:

- Institute a 36% APR cap, inclusive of all fees and charges, including those fees and charges incident to making or renewing a payday loan;

- Ensure that payday lenders are not evading the rate cap by including an anti-evasion provision; and

- Provide meaningful recourse for borrowers who are issued loans that violate the rate cap or other included protections.

A 36% rate cap is the right legislative move to end predatory lending

The most effective way to prevent the fee drain and consequent harms of payday loans is for states to enact a rate cap of about 36% or less. These rate caps allow states to prevent and enforce unsafe lending practices, whether online or in a store.

Active-duty military families are protected with a 36% rate cap under the federal Military Lending Act, but veterans remain unprotected and are still subject to 400% interest predatory lending in Louisiana. Currently, 18 states and the District of Columbia have enacted rate caps of about 36%, saving billions of dollars annually in abusive fees.

Research shows these states have achieved a combined savings of $2.2 billion per year in fees that would otherwise be paid to predatory lenders. Former borrowers report a variety of strategies to address cash flow shortfalls at a fraction of the cost of payday loans, and without the financial damage caused by payday lending including:

- Mainstream Products

A number of other sources of emergency liquidity are becoming more prevalent to help cash strapped consumers. These include credit cards, lines of credit, checking, and savings accounts.

- Installment Loans

Installment loans are marketed to subprime borrowers, many of whom may also be targeted by payday lenders. These loans are substantially less expensive than payday loans, though they are certainly not without their concerns, including high rates of repeat lending and rates up to the states’ interest rate caps of 36%, as well as add‐on products that significantly increase the effective interest rate. It is recommended that states regulate these products to ensure that effective interest rates are also capped.

- Other Products and Services

These include family donations, employer and non‐profit employer‐based emergency loan programs, loans from religious institutions, and extended payment plans from suppliers of consumer services.

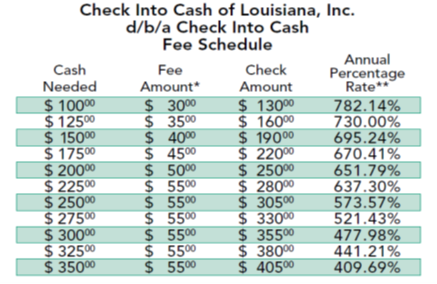

Figure 1: Check Into Cash, a Tennessee-based payday lender, is charging Louisianans over 700% APR under the Deferred Presentment and Small Loan Act.

Figure 2: Speedy Cash, a Texas-based payday lender, is charging Louisianans almost 700% APR under the Deferred Presentment and Small Loan Act.

The Louisiana Budget Project partnered with the Center for Responsible Lending for its work on payday lending during the 2022 Louisiana legislative session.